Every April, millions of salaried Indians face the same question: which tax regime should I choose? With the Union Budget 2025 reshaping the New Tax Regime significantly, the math has changed, and for most taxpayers, it has changed in their favour. But “most” does not mean “all.”

This guide breaks down the exact income tax liability for CTC brackets of ₹15 lakh, ₹20 lakh, ₹30 lakh, and ₹50 lakh under both the New and Old Tax Regimes for FY 2025-26 (AY 2026-27), so you can walk away knowing exactly where you stand, not just in theory, but in rupees.

Table of Contents

What Changed in Budget 2025 That Actually Matters

Before diving into the numbers, you need to understand the three changes from Union Budget 2025 that directly affect your tax outgo:

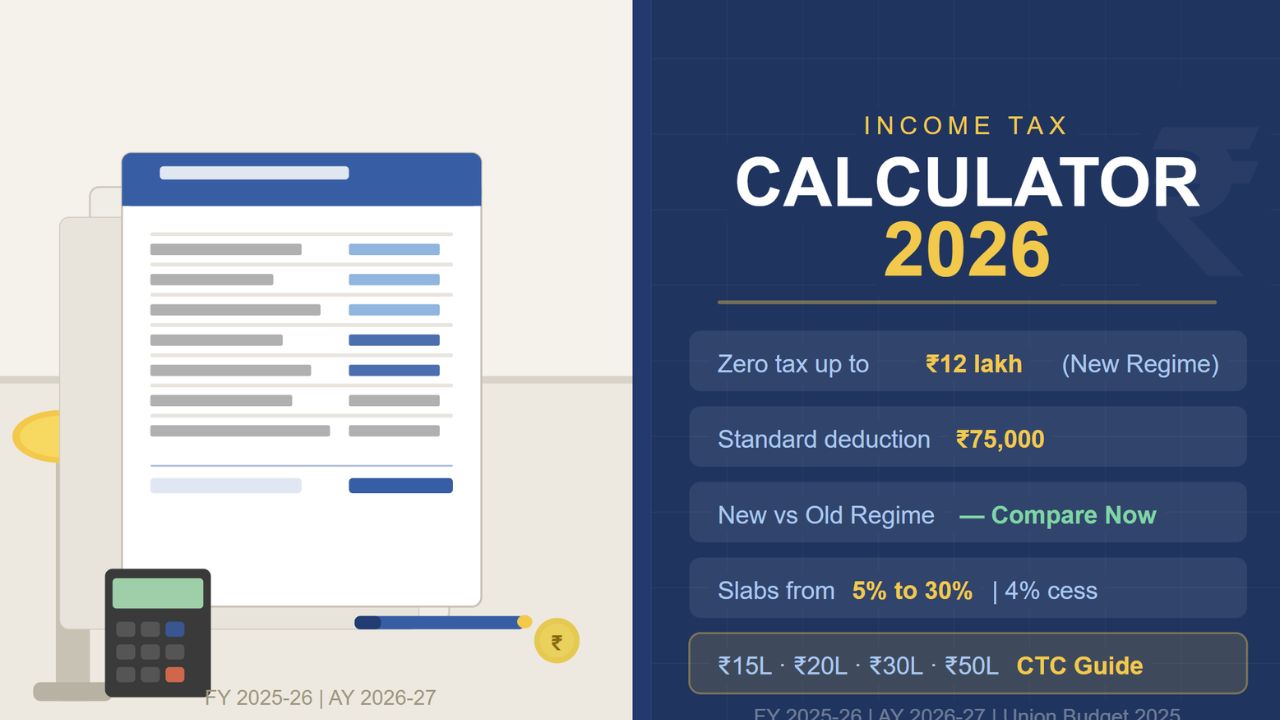

1. Zero tax up to ₹12 lakh (New Regime). The Section 87A rebate was raised to ₹60,000, effectively making income up to ₹12 lakh completely tax-free under the New Regime. This is a massive jump from the earlier ₹7 lakh limit.

2. Higher standard deduction for salaried employees. The standard deduction under the New Tax Regime is ₹75,000 for salaried employees, while it remains ₹50,000 under the Old Regime. This means salaried individuals in the new regime effectively pay zero tax on income up to ₹12.75 lakh.

3. Revised slab structure The new tax regime slabs for FY 2025-26 are: up to ₹4 lakh — Nil, ₹4–8 lakh — 5%, ₹8–12 lakh — 10%, ₹12–16 lakh — 15%, ₹16–20 lakh — 20%, ₹20–24 lakh — 25%, and above ₹24 lakh — 30%. Notably, the 30% rate previously kicked in above ₹15 lakh. Now, it only starts beyond ₹24 lakh — a major structural relief for middle- and upper-middle-income earners.

New Tax Regime vs Old Tax Regime — The Core Difference

The choice between the two regimes essentially comes down to one question: how much can you legitimately claim in deductions?

The Old Tax Regime allows a wide range of deductions, Section 80C (up to ₹1.5 lakh for investments in PPF, ELSS, LIC, EPF, home loan principal), Section 80D (health insurance premiums), HRA exemption, home loan interest under Section 24(b), and NPS contributions under Section 80CCD(1B), among others. These can add up meaningfully.

The New Tax Regime removes almost all of these, but compensates with substantially lower slab rates, a higher standard deduction, and a far more generous rebate threshold.

As a general rule, you need ₹5–8 lakh or more in total deductions for the Old Regime to beat the New Regime.

Income Tax Slabs at a Glance: New vs Old Regime (FY 2025-26)

New Tax Regime Slabs (FY 2025-26):

| Income Slab | Tax Rate |

|---|---|

| Up to ₹4 lakh | Nil |

| ₹4 lakh – ₹8 lakh | 5% |

| ₹8 lakh – ₹12 lakh | 10% |

| ₹12 lakh – ₹16 lakh | 15% |

| ₹16 lakh – ₹20 lakh | 20% |

| ₹20 lakh – ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

Old Tax Regime Slabs (for individuals below 60 years):

| Income Slab | Tax Rate |

|---|---|

| Up to ₹2.5 lakh | Nil |

| ₹2.5 lakh – ₹5 lakh | 5% |

| ₹5 lakh – ₹10 lakh | 20% |

| Above ₹10 lakh | 30% |

A 4% Health and Education Cess applies on the total tax under both regimes. Surcharge kicks in once income exceeds ₹50 lakh. The maximum surcharge under the New Tax Regime is capped at 25%, whereas under the Old Regime it can go as high as 37%, which historically pushed effective tax rates for high earners to over 42%.

Tax Liability Comparison: ₹15 Lakh CTC

For a salaried individual with a gross CTC of ₹15 lakh:

Under the New Tax Regime: After deducting the standard deduction of ₹75,000, the taxable income is ₹14.25 lakh.

Tax calculation:

- ₹0–₹4L: Nil

- ₹4L–₹8L: 5% = ₹20,000

- ₹8L–₹12L: 10% = ₹40,000

- ₹12L–₹14.25L: 15% = ₹33,750

Total base tax: ₹93,750 + 4% cess = ₹97,500

Under the New Tax Regime, for a gross annual income of ₹15 lakh, the total tax liability works out to ₹97,500, significantly lower than the Old Regime in most scenarios.

Under the Old Tax Regime (with typical deductions): Assuming standard deduction of ₹50,000 + Section 80C of ₹1.5 lakh + Section 80D of ₹25,000, total deductions come to ₹2.25 lakh. Net taxable income: ₹12.75 lakh.

Tax calculation:

- ₹2.5L–₹5L: 5% = ₹12,500

- ₹5L–₹10L: 20% = ₹1,00,000

- ₹10L–₹12.75L: 30% = ₹82,500

Total base tax: ₹1,95,000 + 4% cess = ₹2,02,800

Verdict at ₹15L: The New Regime saves approximately ₹1,05,300 even with moderate deductions in the Old Regime. To make the Old Regime competitive at this income level, your total tax-saving deductions would need to exceed ₹5,44,000, a high bar for most salaried employees.

Tax Liability Comparison: ₹20 Lakh CTC

Under the New Tax Regime: After standard deduction, taxable income = ₹19.25 lakh.

Tax calculation:

- ₹0–₹4L: Nil

- ₹4L–₹8L: 5% = ₹20,000

- ₹8L–₹12L: 10% = ₹40,000

- ₹12L–₹16L: 15% = ₹60,000

- ₹16L–₹19.25L: 20% = ₹65,000

Total base tax: ₹1,85,000 + 4% cess = ₹1,92,400

For a ₹20 lakh salary under the New Regime, the final tax liability comes to ₹1,92,400.

Under the Old Tax Regime (with typical deductions): With deductions of ₹2.25 lakh, taxable income = ₹17.75 lakh. This puts a large chunk in the 30% bracket, resulting in a significantly higher tax outgo, typically around ₹3.5 lakh or more, including cess.

Verdict at ₹20L: At ₹20 lakh income, to make the Old Regime beneficial, your total tax-saving investments and deductions would need to exceed ₹7,08,500. Very few salaried individuals without a home loan can cross this threshold.

Tax Liability Comparison: ₹30 Lakh CTC

At this income level, more deductions become accessible, particularly home loan interest under Section 24(b), which can go up to ₹2 lakh for self-occupied property.

Under the New Tax Regime: After standard deduction, taxable income = ₹29.25 lakh.

Tax calculation:

- ₹0–₹4L: Nil

- ₹4L–₹8L: 5% = ₹20,000

- ₹8L–₹12L: 10% = ₹40,000

- ₹12L–₹16L: 15% = ₹60,000

- ₹16L–₹20L: 20% = ₹80,000

- ₹20L–₹24L: 25% = ₹1,00,000

- ₹24L–₹29.25L: 30% = ₹1,57,500

Total base tax: ₹4,57,500 + 4% cess = ₹4,75,800 (approx)

Under the Old Tax Regime (with aggressive deductions): Assuming total deductions of ₹3.75 lakh (80C ₹1.5L + home loan interest ₹2L + 80D ₹25,000), taxable income = ₹26.25 lakh. With the old slab structure, nearly everything above ₹10L falls under 30%, leading to roughly ₹5.5–6 lakh in tax including cess.

Verdict at ₹30L: The New Regime still wins for most. For income above ₹25 lakh, the Old Regime becomes beneficial only when total deductions exceed ₹8 lakh. This is achievable for someone with a substantial home loan, maximum 80C utilisation, NPS contributions, and high health insurance premiums — but it requires deliberate and disciplined financial planning.

Tax Liability Comparison: ₹50 Lakh CTC

This is where surcharge enters the picture, and the comparison gets nuanced.

Under the New Tax Regime: After standard deduction, taxable income = ₹49.25 lakh.

Tax slab calculation results in a base tax of approximately ₹11,32,500, before cess. Since income is just under ₹50 lakh (post-standard deduction), surcharge may or may not apply depending on gross income, worth checking with a tax professional.

Adding 4% cess: total tax approximately ₹11,77,800 (approx).

Under the Old Tax Regime: Even with deductions of ₹4–5 lakh, taxable income will be around ₹45 lakh, still attracting 30% on a majority of income, plus a 10% surcharge on incomes above ₹50 lakh. Under the Old Regime, the maximum surcharge rate reaches 37%, pushing the effective tax rate past 42% for incomes above ₹5 crore.

Verdict at ₹50L: At this level, the New Regime’s surcharge cap of 25% becomes a critical advantage for some taxpayers. The maths here gets complex — employer NPS contributions under Section 80CCD(2), HRA exemption, and home loan interest can make the Old Regime viable, but it requires calculation. Both regimes deserve a side-by-side run through a tax calculator at this income level.

Deductions Still Available Under the New Tax Regime

The New Regime is not entirely bare-bones. Under the New Regime, the following benefits are still available: enhanced standard deduction of ₹75,000; family pension deduction of ₹25,000; employer’s NPS contribution deduction under Section 80CCD(2) up to 14% of basic salary; EPF interest on contributions up to ₹2.5 lakh annually; gratuity exemption at retirement; and life insurance maturity proceeds under Section 10(10D) subject to conditions.

The employer NPS contribution deduction under Section 80CCD(2) is especially powerful and often underused. It reduces taxable income without requiring the employee to make any out-of-pocket investment.

When Does the Old Regime Still Make Sense?

Despite the New Regime’s obvious appeal, the Old Regime remains the better choice in specific situations:

If you have a large home loan: Section 24(b) allows up to ₹2 lakh in interest deduction on a self-occupied property. Combined with Section 80C for the principal repayment component, homeowners can claim ₹3–3.5 lakh from this single loan alone.

If you live in a metro and pay high rent: HRA exemption under the Old Regime can be substantial, particularly in cities like Mumbai, Delhi, Bengaluru, and Chennai — where rent constitutes a major portion of income.

If you aggressively invest: Taxpayers who maximise Section 80C (₹1.5 lakh), add ₹50,000 via Section 80CCD(1B) for NPS, pay health insurance for parents (up to ₹50,000 deductible under 80D for senior citizen parents), and have interest income in savings accounts can stack deductions well beyond ₹3.75–4 lakh.

If you are a senior citizen: Senior citizens in particular may benefit more under the Old Regime through Section 80TTB, which allows a ₹50,000 deduction on interest income.

A Quick Break-Even Guide

Here is a straightforward way to decide without doing full calculations:

Income ₹12.75 lakh or below → New Regime always wins. Zero tax after the standard deduction and the Section 87A rebate. No contest.

Income ₹15–20 lakh → New Regime wins unless deductions exceed ₹5.5–7 lakh. Very few salaried employees without a home loan can cross this threshold.

Income ₹20–30 lakh → New Regime wins for most, but home loan owners should recalculate. A home loan plus maximum 80C and NPS can start tilting the balance.

Income ₹30–50 lakh → Genuinely compute both. At this level, every lakh in deductions matters. Employer NPS contribution, HRA, home loan interest, and 80D together can make the Old Regime competitive.

Income above ₹50 lakh → Factor in surcharge. The New Regime’s 25% surcharge cap versus the Old Regime’s 37% cap can be decisive for very high earners.

How to Calculate Your Tax in 5 Steps

- Start with your gross CTC. Separate actual salary from reimbursements, perquisites, and employer contributions.

- Subtract the standard deduction — ₹75,000 (New Regime) or ₹50,000 (Old Regime).

- Under Old Regime: Subtract eligible deductions — 80C, 80D, HRA, home loan interest, 80CCD(1B), etc.

- Apply applicable slab rates to your net taxable income.

- Add 4% cess on the calculated tax. If income exceeds ₹50 lakh, add the applicable surcharge before the cess.

The ITR filing deadline for FY 2025-26 is 31 July 2026 for most salaried individuals. Around 88% of taxpayers have already moved to the New Tax Regime, reflecting its growing acceptance.

The Bottom Line

For the majority of salaried Indians, the New Tax Regime in FY 2025-26 is the clear winner, especially at income levels up to ₹20 lakh and for those without significant home loans or heavy deduction portfolios. The revised slabs, the generous ₹12 lakh zero-tax threshold, and the higher standard deduction collectively represent a meaningful structural shift in India’s personal tax framework.

However, the Old Regime is not dead. Taxpayers with home loans, substantial 80C commitments, senior citizen parents, and high HRA should run the numbers carefully; they may still find meaningful savings in the older structure.

The key takeaway: don’t assume, calculate. Use a reliable income tax calculator, enter your actual figures, and let the arithmetic decide, not assumptions or habit.