Most investors think of the Public Provident Fund as a tax-saving tool they fill up in March and forget. That framing does the scheme a serious disservice. PPF is not a tax instrument with a savings component attached. It is a compounding engine with a tax benefit attached, and if you understand the difference, you will approach it very differently.

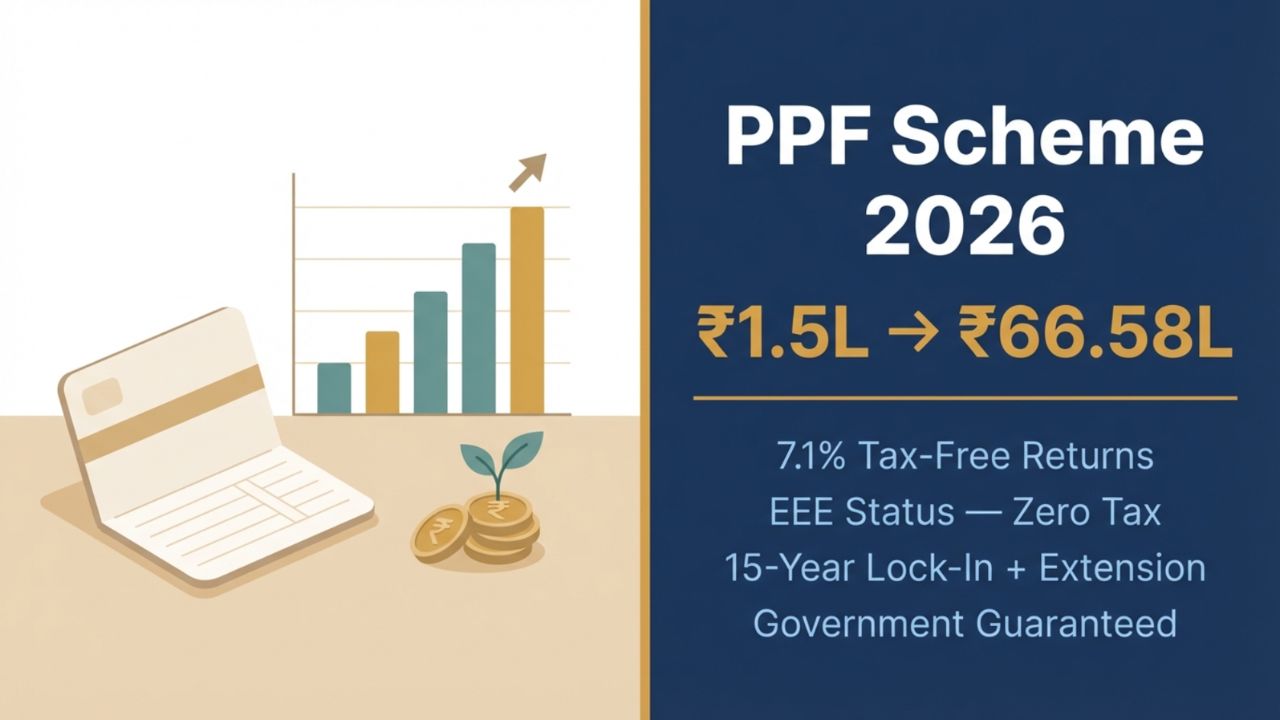

If you invest the maximum allowed amount of ₹1.5 lakh per year at 7.1% per annum and extend the account by one 5-year block beyond the standard 15-year tenure, the maturity amount jumps to approximately ₹66.58 lakh. The compounding effect accelerates dramatically in the later years, from Year 16 onwards, the interest earned per year actually exceeds your annual deposit.

That is ₹30 lakh in invested capital turning into ₹66.58 lakh, entirely tax-free, without any market exposure, no fund manager risk, and backed by the sovereign guarantee of the Government of India. This guide explains exactly how it works, what the rules are in 2026, and how to extract maximum value from every rupee you put in.

Table of Contents

What Is PPF and Why Does It Still Matter in 2026?

The Public Provident Fund was introduced in 1968 by the National Savings Institute under the Ministry of Finance. Over five decades later, it remains one of the most structurally sound savings instruments available to Indian residents, not because it offers the highest returns, but because of what it combines: government-backed safety, an interest rate that consistently beats inflation on a post-tax basis, and the rare triple tax exemption that no other instrument matches in its entirety.

The PPF interest rate for Q1 FY 2026-27 remains at 7.1% per annum, compounded annually, and credited on March 31 each year. Interest is calculated monthly based on the lowest balance between the 5th and the last day of each month.

At 7.1% tax-free, the effective pre-tax equivalent return for someone in the 30% tax bracket is approximately 10.1%. Most fixed deposits, debt mutual funds, and even some hybrid instruments cannot match this on a post-tax, risk-adjusted basis. In a world drowning in investment noise, PPF remains stubbornly relevant.

The Numbers That Make the Case

Let us start with the headline and work backwards to understand it.

At 15 years (standard tenure): Investing ₹1.5 lakh annually at 7.1% per annum yields a maturity corpus of approximately ₹40.68 lakh. Your total investment is ₹22.5 lakh. The remaining ₹18.18 lakh is pure tax-free interest.

At 20 years (one 5-year extension with continued deposits): The maturity amount grows to approximately ₹66.58 lakh. The compounding effect accelerates dramatically, from Year 16 onwards, annual interest credited exceeds your annual deposit of ₹1.5 lakh. Total investment across 20 years: ₹30 lakh. Tax-free interest earned: ₹36.58 lakh.

At 25 years (two 5-year extensions with continued deposits): By continuing to invest the full ₹1.5 lakh annually for 25 years, your savings can grow to over ₹1 crore, specifically around ₹1.03 crore at the current interest rate.

The mathematics here are extraordinary. Your invested capital from Year 15 to Year 25 is only an additional ₹15 lakh. Yet the corpus nearly doubles, from ₹40.68 lakh to over ₹1 crore. This is compounding doing its heaviest lifting on a large base, and it is the single strongest argument for never closing a PPF account at exactly 15 years.

The EEE Status: The Tax Advantage No Other Instrument Fully Matches

PPF enjoys what is called EEE, Exempt-Exempt-Exempt, tax treatment. Every layer of your investment is shielded from tax:

Layer 1, Investment is tax-deductible: Contributions up to ₹1.5 lakh per year qualify for deduction under Section 80C of the Income Tax Act. This applies only under the Old Tax Regime. Under the New Tax Regime, the Section 80C deduction is not available, however, the interest income and maturity proceeds remain fully tax-free regardless of which regime you choose.

Layer 2, Interest earned is tax-free: Unlike fixed deposits where interest is taxed as income every year, PPF interest compounds tax-free inside the account. There is no TDS, no annual tax liability, and no ITR entry required for interest accrual.

Layer 3, Maturity proceeds are fully exempt: The entire corpus, principal plus accumulated interest, is received completely tax-free. There is no capital gains tax, no surcharge, and no cess at the time of withdrawal.

This triple shield is why a 7.1% PPF return comfortably outperforms a 7.5% fixed deposit for anyone in the 20% or 30% tax bracket on a real, after-tax basis.

PPF Rules in 2026: Everything You Need to Know

Who Can Open a PPF Account

Any resident Indian individual can open a PPF account. Only Indian residents can open a PPF account. HUFs, NRIs, and Bodies of Individuals are not eligible. Joint accounts are not permitted, the account can only be held in one person’s name. However, an investor can hold only one account in their own name, or open a second account on behalf of a minor child.

An important planning nuance: if you deposit ₹1.5 lakh in your own account, you cannot deposit additionally in the minor’s account in the same year. The ₹1.5 lakh limit is shared across both accounts combined. For families where a spouse also invests in PPF, their account is entirely independent with its own separate ₹1.5 lakh limit, effectively doubling the family’s annual PPF capacity to ₹3 lakh.

Deposit Rules

Minimum: ₹500 per financial year. Missing even one year makes the account inactive, requiring a ₹50 penalty per missed year plus the minimum deposit to reactivate.

Maximum: ₹1.5 lakh per financial year, across lump sum or up to 12 instalments. Any amount deposited beyond ₹1.5 lakh will be rejected automatically and earn no interest.

Timing: Deposit before the 5th of every month to earn interest for that month. For lump-sum annual investors, depositing the full amount before April 5th ensures interest on the entire amount for all 12 months of the financial year. Early investment timing can boost cumulative returns by up to ₹30,000–₹40,000 over 15 years, simply through disciplined timing.

The Lock-In Period and Maturity

The lock-in period is 15 years, calculated from the end of the financial year in which the account was opened, not from the calendar date of the first deposit. This means if you open an account in October 2026, the tenure begins from March 31, 2027, and the account matures on April 1, 2042. Effectively, you make 16 annual contributions over this period, not 15.

Partial Withdrawals

Partial withdrawals are permitted from the 7th financial year onwards. The maximum amount you can withdraw is up to 50% of the balance at the end of the 4th year preceding the year of withdrawal, or the preceding year’s balance, whichever is lower. Only one withdrawal is permitted per financial year.

This liquidity window makes PPF meaningfully more accessible than it appears. An investor who opened an account in April 2020 becomes eligible for partial withdrawals from FY 2026-27, right now. The withdrawn amount remains tax-free.

The Loan Facility

A loan against the PPF account is available from the 3rd financial year to the end of the 6th year. The maximum loan amount is 25% of the balance at the end of the 2nd year preceding the loan application year. The loan must be repaid within 36 months; interest is charged at 1% over the PPF interest rate if repaid within 36 months, and 6% if not.

The loan facility is particularly useful for short-term cash crunches in the early years before partial withdrawals become available. Unlike a personal loan, the interest rate is capped and modest, and importantly, it keeps your PPF balance intact and compounding.

Premature Closure

Premature closure is allowed after 5 years, but only under specific conditions, serious illness of the account holder, spouse, or dependent children; or higher education needs. A 1% interest penalty applies, meaning the interest earned is reduced by 1% across the entire tenure.

In practice, premature closure should be a last resort. The 1% penalty over 10+ years can amount to a significant reduction in corpus.

The Extension Strategy: Where PPF Becomes Truly Powerful

Most investors close their PPF account at 15 years, take the maturity amount, and move on. This is arguably the biggest wealth-creation mistake in personal finance.

After the 15-year lock-in, you have three choices:

Option 1, Withdraw fully and close: The entire corpus is paid out tax-free. Simple, clean, final.

Option 2, Extend with continued contributions: Submit Form H within one year of maturity. You continue depositing up to ₹1.5 lakh annually, retaining the Section 80C deduction (under Old Regime), and the balance continues compounding. Partial withdrawals remain subject to the standard rule.

Option 3, Extend without contributions: You can let the account remain open without depositing further, and it will continue earning tax-free interest at the prevailing PPF rate. During the extension period without contributions, you can make partial withdrawals of any amount once per year without restrictions, making this option very flexible for retirement planning.

Option 3 is particularly powerful for retirees or near-retirees. Your accumulated corpus of ₹40+ lakh sits in a government-backed account earning 7.1% tax-free, and you can draw from it annually with complete flexibility. No market risk, no fund manager, no tax. It functions as a personal government-backed annuity.

The Minor Child Strategy: Building a Corpus From Birth

Parents or legal guardians can open and operate a PPF account on behalf of a minor child from birth. If you open a PPF account for a 5-year-old daughter, the account matures 15 years later when she is 20, precisely timed for higher education expenses or early career financial support.

The mathematics of starting early is compelling. A PPF account opened at birth and invested for 15 years builds the same ₹40.68 lakh corpus, but the child receives it tax-free at age 15, with the option to extend further into their working years. Starting at birth and extending to 20 years creates a ₹66.58 lakh tax-free corpus before the child turns 21.

The shared ₹1.5 lakh annual limit across parent and child accounts is the key constraint to plan around. Families where both spouses are earning can effectively have three active PPF accounts, one each in the spouses’ names (₹1.5 lakh each, fully independent) and one in the child’s name (shared limit with one parent’s account).

PPF vs. Other Fixed-Income Options: The Honest Comparison

The most common challenge to PPF is that bank fixed deposits or debt funds sometimes offer higher nominal rates. Here is the full picture:

A bank FD at 7.5% for a 30% taxpayer yields an effective post-tax return of 5.25%. A PPF at 7.1% yields 7.1% post-tax, every single year, for up to 25+ years with compounding. The PPF wins by approximately 185 basis points on a post-tax basis, every year, which compounds into an enormous difference over 15–20 years.

Against debt mutual funds, the comparison is nuanced. Debt funds can be more liquid and offer market-linked upside, but they are subject to income tax at applicable slab rates for most investors since 2023. The tax-free certainty of PPF, combined with its government guarantee, gives it a structural advantage for the conservative, long-term portion of any portfolio.

For someone in the 30% tax bracket, PPF’s 7.1% tax-free return is equivalent to a pre-tax return of approximately 9.8%, better than most fixed deposits and debt funds on a post-tax basis.

How to Open a PPF Account in 2026

PPF accounts can now be opened using Aadhaar-based biometric eKYC authentication, with funds deposited and withdrawn using this paperless facility. The process is available online through most major banks, SBI, HDFC, ICICI, Axis, PNB, and through post offices.

For online opening via net banking, the process takes under 10 minutes. You need your Aadhaar, PAN, a linked savings account, and a first deposit of at least ₹500. The PPF account number is generated immediately, and you can start transacting the same day.

For post office opening, submit Form 1 along with Aadhaar, PAN, two passport-size photographs, and the first deposit. A passbook is issued upon account creation.

You can transfer your PPF account from a bank to a post office, from a post office to a bank, and between branches of the same bank, by submitting a transfer request at the home branch. This flexibility means you are never locked to a single institution for 15 years.

The One Mistake That Costs Most PPF Investors Thousands

Depositing in March to save tax is the single most common and most expensive habit among PPF investors. Every March deposit earns interest for only one month of the financial year. Moved to April, before the 5th, the same deposit earns for all 12 months.

Over 15 years of consistently depositing in March versus April, the difference in final corpus is significant. Over 20 years with the 5-year extension, it is even larger. The money saved is identical. The tax benefit is identical. Only the timing changes, and so does the outcome.

Set a standing instruction. Schedule the transfer. Treat it like a rent payment that does not negotiate on dates.

Who Should Invest in PPF

PPF is not for everyone’s entire investment portfolio, and it should not be. But it belongs in nearly every Indian investor’s plan as a core foundation component.

It is ideal for the salaried investor under the Old Tax Regime who wants to maximise Section 80C with a risk-free, liquid-on-maturity option. It is ideal for the conservative long-term saver building a retirement floor that requires no market monitoring. It is ideal for parents building a corpus for a child’s education or early adult life. It is ideal for the high-income professional who wants a guaranteed, government-backed instrument as a counterweight to equity exposure.

It is not ideal as the only investment. At 7.1%, PPF will not keep pace with the real cost of ambitious life goals like early retirement or wealth creation above inflation on an absolute basis. Pair it with equity, mutual funds, direct stocks, or NPS, and PPF becomes the anchor that lets you hold the rest of the portfolio through market turbulence without panic.

The ₹66.58 lakh at 20 years is not a promise. It is a projection at a constant 7.1% rate that the government reviews quarterly. The rate has held at 7.1% since April 2020, six full years of stability. But the long-term investor should build plans around the structural properties of PPF, government backing, EEE status, disciplined lock-in, rather than assuming any specific rate persists across two decades.

What does not change is this: PPF is the most tax-efficient, risk-free compounding vehicle available to an Indian retail investor. Used with discipline, maximum deposits, early-in-the-month timing, extensions beyond 15 years, it builds wealth quietly, reliably, and completely free of tax. Start early, stay consistent, and let time do the work.